The Medicare Part B Late Enrollment Penalty, Explained

The short answer

The Part B late enrollment penalty adds 10% to your monthly premium for each full 12-month period you were eligible for Part B but didn't enroll and had no creditable coverage. It isn't a one-time fee - it's added to your premium for as long as you have Medicare, and there's no cap. It's avoidable: enroll during your Initial Enrollment Period, or within 8 months of losing qualifying employer coverage.

Most Medicare penalties are avoidable - which is exactly why it's worth understanding how they work before you're the one paying one. The Part B late enrollment penalty is one of the most misunderstood, mostly because of one detail: it isn't a one-time fee. It's added to your monthly premium for as long as you have Medicare.

Here's how it actually works.

Who This Applies To

The Part B penalty can apply to you if:

You didn't sign up for Part B when you were first eligible during your Initial Enrollment Period, and

You didn't have other "creditable coverage" (generally, coverage through a current employer or your spouse's current employer) during that time.

If you had qualifying employer coverage and enrolled in Part B within 8 months of that coverage or employment ending (a Special Enrollment Period), you generally won't face a penalty - even if it's been years since your Initial Enrollment Period.

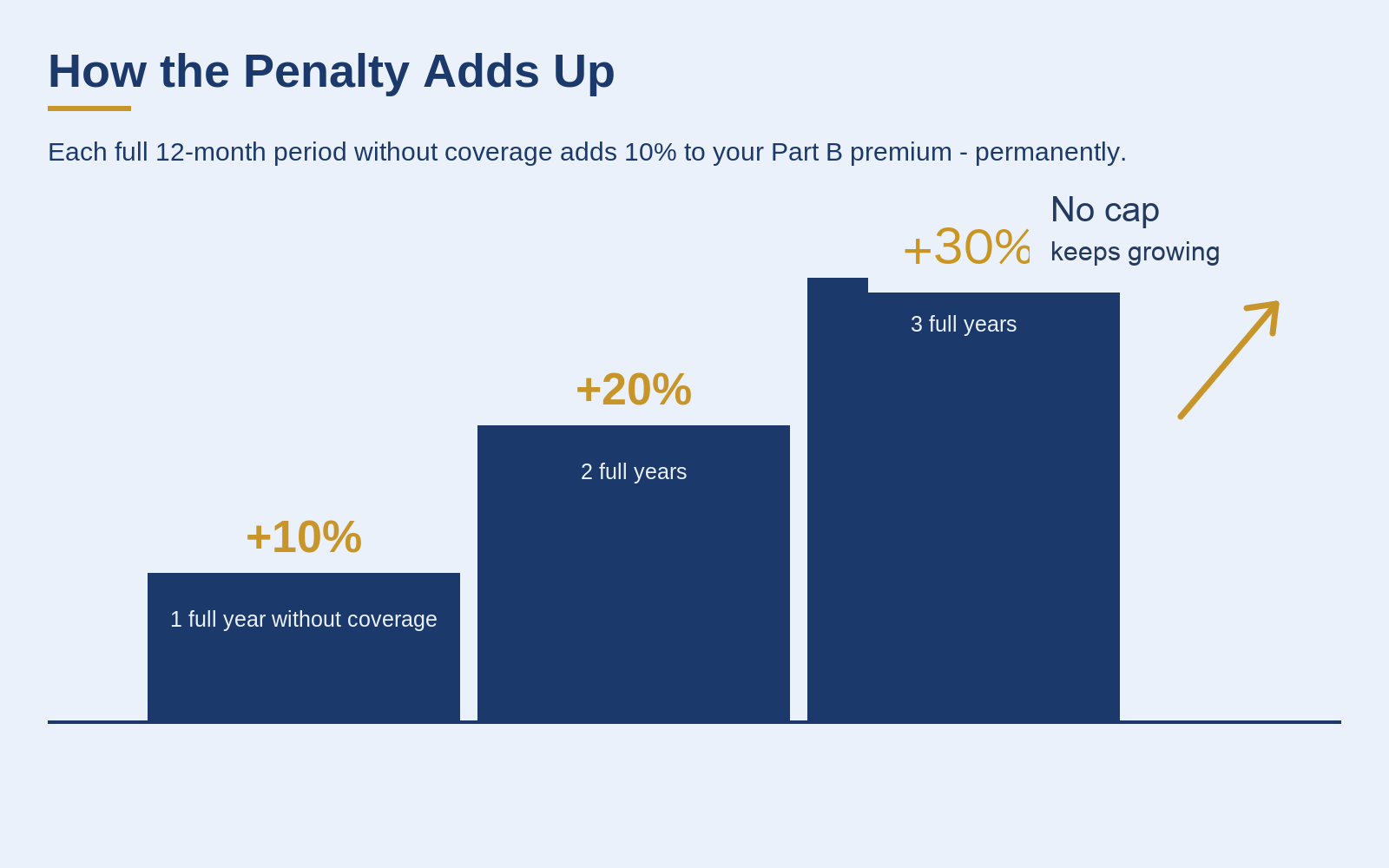

How the Penalty Is Calculated

The Part B penalty is calculated as a percentage, not a flat fee:

For each full 12-month period you were eligible for Part B but didn't enroll (and didn't have creditable coverage), your premium goes up by 10%.

That percentage is added to the standard Part B premium amount for as long as you're enrolled in Medicare - it doesn't expire, and there's no cap on how high it can go if you wait long enough. For the current standard Part B premium amount used to calculate what a specific percentage translates to in dollars, see our companion article, How Much Does Medicare Cost in 2026, which we update annually with CMS-verified figures.

Example (illustrative, not dollar-based): if you were eligible for Part B for 2 full years before enrolling and had no creditable coverage during that time, your penalty would be 20% (2 x 10%) added to the standard premium, for life.

Why This Penalty Exists

Medicare's enrollment penalty structure is designed to encourage people to enroll when they first become eligible, rather than waiting until they need care. Without it, people could theoretically skip Part B while healthy and enroll only once they need expensive treatment - which would undermine how the overall insurance pool is priced for everyone.

How to Avoid It

Enroll during your Initial Enrollment Period if you don't have other creditable coverage. (See our companion article, Medicare Enrollment Periods Explained, for exact IEP timing.)

If you have employer coverage, confirm with your HR department or benefits administrator that it qualifies as creditable coverage under Medicare's definition - not all employer plans automatically do, especially at smaller employers.

Enroll within 8 months of losing employer coverage using your Special Enrollment Period, even if that's well past your original Initial Enrollment Period.

Don't confuse COBRA or retiree coverage with active employer coverage - these generally do NOT count as creditable coverage for avoiding the Part B penalty, which is one of the most common and costly mix-ups we see.

What About the Part D Penalty?

Part D (prescription drug coverage) has its own separate late enrollment penalty, calculated differently (based on the number of months without Part D or other creditable drug coverage, applied to a national base premium that changes each year). If you're weighing whether to delay Part D, that's worth its own conversation - the rules aren't identical to Part B's.

The Bottom Line

The Part B penalty isn't designed to be punitive for its own sake - it exists to keep the system fair for everyone paying in. But because it compounds and never expires, it's one of the more expensive mistakes to make by accident. If there's any uncertainty about whether your current coverage qualifies as creditable, that's worth a 10-minute conversation before your enrollment window closes, not after.

Not sure if your coverage qualifies as creditable, or whether you're at risk of a penalty? Call the AdviseCare Insurance team at (813) 544-7066 or book a no-cost, no-obligation call. We'll help you figure out exactly where you stand.

Frequently Asked Questions

How is the Medicare Part B late enrollment penalty calculated?

For each full 12-month period you were eligible for Part B but didn't enroll and didn't have creditable coverage, your premium goes up by 10%. That percentage is added to the standard Part B premium amount for as long as you're enrolled in Medicare. For example, waiting 2 full years without creditable coverage means a 20% penalty added to the standard premium, for life.

Does the Part B penalty ever go away?

No - it isn't a one-time fee. The penalty is added to your monthly premium for as long as you have Part B, it doesn't expire, and there's no cap on how high it can go if you wait long enough to enroll.

Does COBRA count as creditable coverage for avoiding the Part B penalty?

Generally no. COBRA and retiree coverage do not count as active employer coverage for avoiding the Part B penalty - this is one of the most common and costly mix-ups. Creditable coverage generally means coverage through a current employer or your spouse's current employer.

How do I avoid the Part B late enrollment penalty?

Enroll during your Initial Enrollment Period if you don't have other creditable coverage. If you have employer coverage, confirm with your HR department that it qualifies as creditable under Medicare's definition. And if you lose employer coverage, enroll within your 8-month Special Enrollment Period - even if that's well past your original Initial Enrollment Period.