Medicare Supplement Plan G vs. Plan N: What's the Difference?

The short answer

Plan G covers every major Medigap benefit category except the annual Part B deductible. Plan N covers nearly as much, but adds small copays for some office and ER visits and does not cover Part B excess charges - typically in exchange for a different premium structure. Neither is universally better; the right fit depends on your state, your providers, and how you use care.

If you're comparing Medicare Supplement (Medigap) plans, chances are Plan G and Plan N have both come up. They're the two most commonly chosen Medigap plans today, and for good reason - they offer strong coverage at two different structures. But "strong coverage" isn't the same as "identical," and the differences matter depending on how you use healthcare.

Here's how they actually compare, without the sales pitch.

The Short Version

Both plans cover a large share of the gaps left by Original Medicare. The core difference comes down to this: Plan G covers a couple of cost-sharing categories that Plan N doesn't, and in exchange, Plan N typically has a different premium structure. Neither plan is "better" in the abstract - it depends on your priorities and how often you expect to use care.

What Plan G Covers

Plan G is the most comprehensive Medigap plan currently available to new enrollees (Plan F, which covered even more, is no longer available to people who became eligible for Medicare on or after January 1, 2020). Plan G covers:

Part A coinsurance and hospital costs (up to an additional 365 days after Medicare benefits are used).

Part A hospice care coinsurance or copayment.

Part B coinsurance or copayment.

Blood (first 3 pints).

Part A deductible.

Skilled nursing facility coinsurance.

Part B excess charges (the difference between what a provider charges and Medicare's approved amount, in states where providers are allowed to charge more).

Foreign travel emergency care (up to plan limits).

The one thing Plan G does not cover is the Part B annual deductible - you pay that out of pocket each year before Plan G coverage on Part B services kicks in.

What Plan N Covers

Plan N covers nearly everything Plan G does, with two structural differences:

Plan N does not cover Part B excess charges.

Plan N requires small copayments for some office visits and emergency room visits (a modest copay for doctor visits that don't result in an inpatient admission, and a separate copay for ER visits that don't result in admission).

Otherwise, Plan N covers the same core categories as Plan G: Part A coinsurance and hospital costs, Part A hospice coinsurance, Part B coinsurance (outside the copay exceptions above), blood, Part A deductible, skilled nursing coinsurance, and foreign travel emergency care.

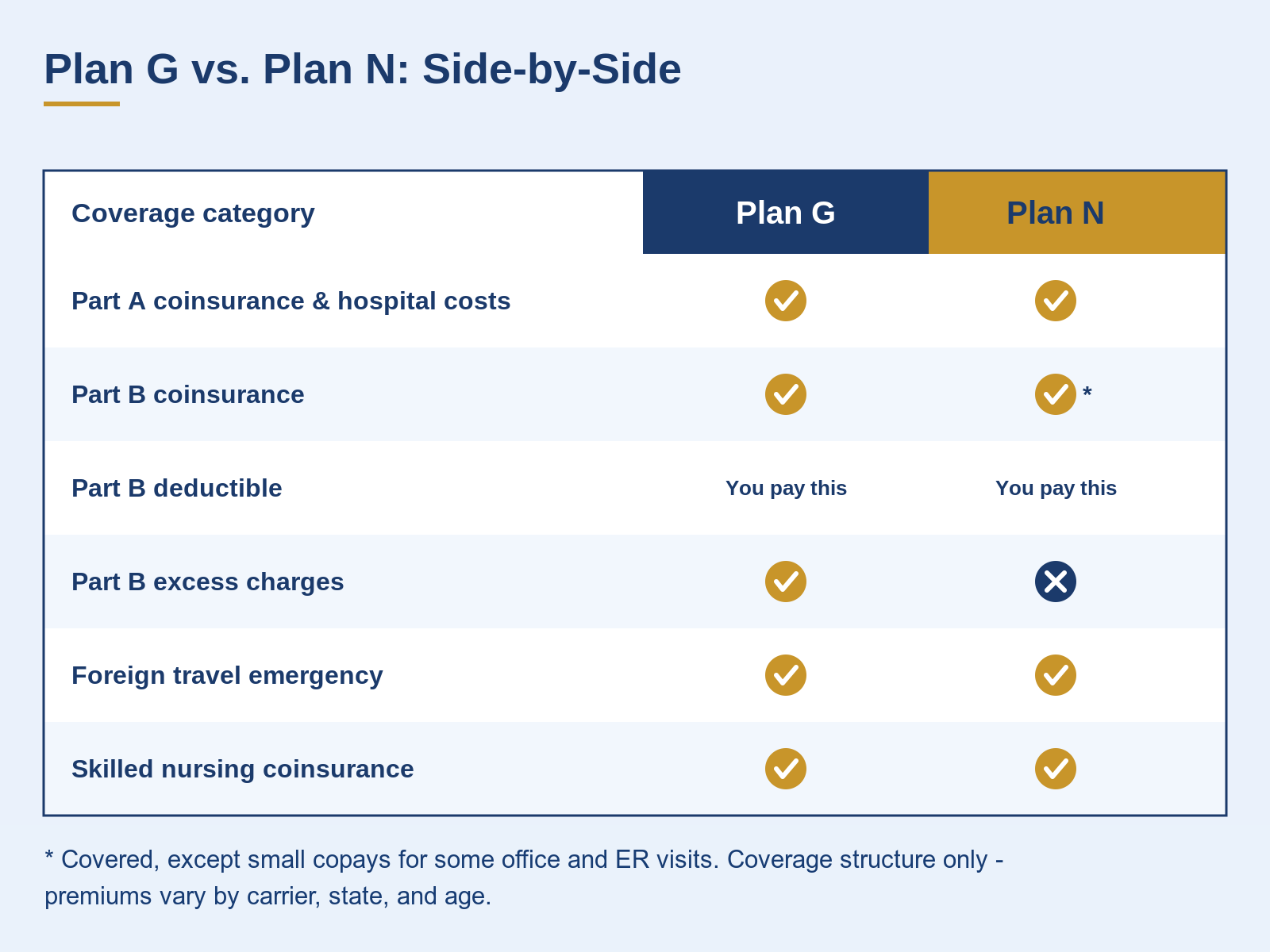

Side-by-Side: Where They Differ

| Coverage Category | Plan G | Plan N |

|---|---|---|

| Part A deductible | Covered | Covered |

| Part A coinsurance / hospital costs | Covered | Covered |

| Part B coinsurance | Covered in full | Covered, except small copays for some office/ER visits |

| Part B excess charges | Covered | Not covered |

| Part B annual deductible | Not covered (you pay this) | Not covered (you pay this) |

| Skilled nursing coinsurance | Covered | Covered |

| Foreign travel emergency | Covered (up to plan limits) | Covered (up to plan limits) |

What "Part B Excess Charges" Actually Means

This is the detail that trips people up. In most states, Medicare-approved providers agree to accept Medicare's approved amount as full payment. But some providers ("non-participating providers") are legally allowed to charge up to 15% more than the Medicare-approved amount for a service - that difference is an "excess charge." Plan G covers it. Plan N doesn't.

Whether this matters to you depends heavily on your state and which providers you see. In many states, excess charges are rare in practice or not legally permitted at all. In others, it's a real consideration.

Which One Should You Consider?

This isn't a question we can answer generically, because the honest answer depends on:

Whether your state allows Part B excess charges, and whether your providers charge them.

How often you expect to see a doctor or visit urgent care/ER in a typical year (Plan N's copays are per-visit).

Your priorities around predictable costs vs. potentially lower premiums.

Premiums for both plans vary by carrier, state, age, and sometimes tobacco use - there's no universal number that applies to everyone, which is exactly why this decision benefits from a real conversation instead of a generic comparison chart.

The Bottom Line

Plan G and Plan N are both strong, well-established Medigap options that solve the same basic problem - filling the gaps Original Medicare leaves open - using slightly different structures. Neither is a wrong choice. The right one is the one that matches how you actually use healthcare and what you want your monthly costs to look like.

Trying to decide between Plan G, Plan N, or another option entirely? Call the AdviseCare Insurance team at (813) 544-7066 or book a no-cost, no-obligation call. We'll walk through what each plan would mean for your specific situation.

- AdviseCare Insurance

Frequently Asked Questions

What is the difference between Medicare Plan G and Plan N?

Plan N covers nearly everything Plan G does, with two structural differences: Plan N does not cover Part B excess charges, and it requires small copayments for some office visits and emergency room visits that don't result in admission. Otherwise both plans cover the same core categories - Part A coinsurance and hospital costs, hospice coinsurance, Part B coinsurance, blood, the Part A deductible, skilled nursing coinsurance, and foreign travel emergency care.

Does Plan G cover the Medicare Part B deductible?

No. The one thing Plan G does not cover is the Part B annual deductible - you pay that out of pocket each year before Plan G coverage on Part B services kicks in. Plan N doesn't cover it either.

What are Medicare Part B excess charges?

In most states, Medicare-approved providers accept Medicare's approved amount as full payment, but some non-participating providers are legally allowed to charge up to 15% more for a service - that difference is an excess charge. Plan G covers it; Plan N doesn't. Whether it matters depends heavily on your state and which providers you see - in many states excess charges are rare in practice or not permitted at all.

Can I still enroll in Medigap Plan F?

Only if you became eligible for Medicare before January 1, 2020. For everyone who became eligible on or after that date, Plan F is no longer available, which makes Plan G the most comprehensive Medigap plan currently open to new enrollees.